Show me the Money

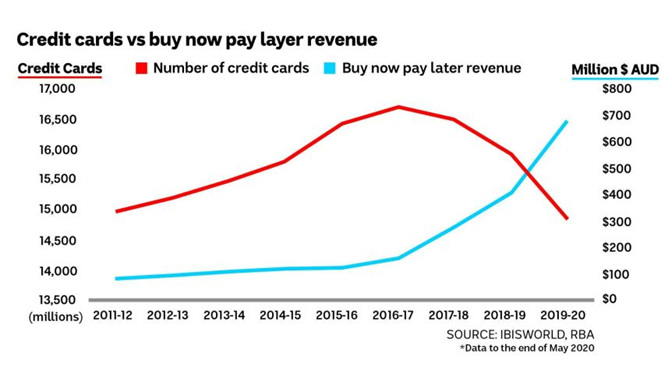

You probably have heard of one of the Buy Now Pay Later (BNPL) platforms: Afterpay, Openpay, ZipPay, Sezzle, Klarna, and lately Paypal?; as the graph above from the Reserve Bank of Australia indicates, credit cards are on the decline and BNPLs are on the rise. I believe the key lies with the fact that unlike credit cards, their main source of revenue is not fees or interest, but charging the merchant for the privilege to use the platform in the hope that it results in more sales at checkout time. They all tinker with the ratio of how much money to extract from merchant vs making the user pay for the product. Why are young people and low-income earners shunning credit cards? Could it be the crippling interest?

Behold the power of compound interest

The fact that there is no hefty interest penalty with BNPLs is appealing to people who have been rejecting credit cards for fear of being pummeled by high interest debt. But then again, some people have started calling them Buy Now, Never Pay due to the high risk in this model versus the Pay Now, Or Else model of credit cards as there is no big stick to the proverbial carrot with BNPLs. But what happens if you don’t pay in this interest-free model? You still get a blotch on your credit score, but it’s not as devastating as being in arrears in your credit card payments and being charged quite a substantial interest. BNPLs also can be nimbler than credit cards due to fact they don’t require an upfront credit check which makes the checkout process more seamless and less people get rejected, thus their user base can grow faster. So how are these BNPLs profitable if business are not getting cash from interest payments and there are no fees (assuming customers pay on time)? It must make revenue somewhere else? The answer is making the merchant pay!

If you are not paying for the product you are the product

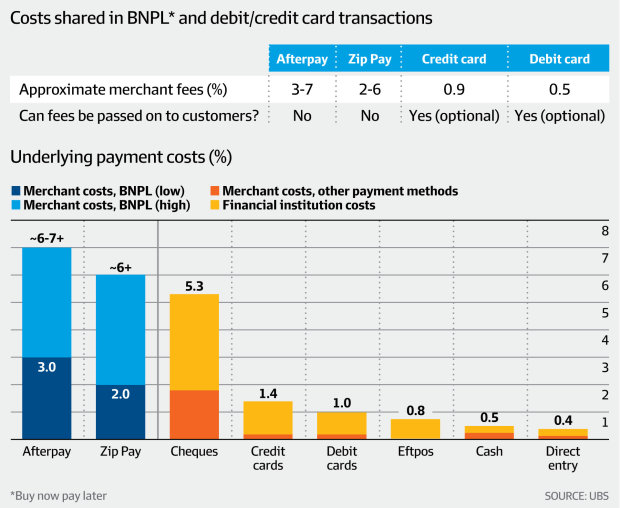

The biggest question being thrown around is if making the merchant pay more is sustainable; won’t they just pass the cost onto the customer anyway? Making the merchant pay upward to 7% of the transaction fee is slightly different to current credit card model. While credit card companies do charge the merchant a fee to use the card, it’s much smaller around 1-3 % range and a healthy sum of their cashflow comes from interest collection and fees. Furthermore, regulation currently favours BNPLs, players like ZIP and Afterpay are not considered a credit provider, thus they can explicitly prevent merchants from passing on the cost. Everyone likes free stuff, and this makes BNPLs popular and this popularity is what the merchants are paying for.

Free me from my own interest

Some Australian banks are realising that the interest-free trend is becoming popular and have released interest-free credit cards for a monthly fee to try and compete, but again they mainly charge the card holder. What is the right ratio of charging the merchant vs charging the user? Being a consultant, I see an opportunity to take the guess work out of the equation with some data driven aggregation of the lending ecosystem, as it only going to get more complicated from here. With so many players out there, it’s confusing to both the merchant and the customer. An Open Data landscape could allow for more data driven decisions by using data points around payment habits and repayment frequency to see which payment product is best suited to you. Merchants can also start visualising whether BNPL is worth the price tag. To take the guess work out of the equation, I would sign up to a bank that would use my data to assist me in my money decisions in this ever growing and fast-paced digital banking landscape. Banks should also be taking the initiative and partnering with BNPLs, following in the footsteps of CBA who have partnered with Klarna.

What are the rules and regulations?

BNPL is nothing new. Interest-free financing has been around for decades; this is just the natural process bringing an old concept into the digital world. Perhaps more and more larger companies will start their own DIY BNPL platform to avoid paying the heavy merchant commission fees and take on the credit risk themselves. According to ASIC, two in five people who buy through BNPL schemes are low-income earners and, of those, two in five are students or part-time workers. It seems like Australia is saturated with BNPL and Australian regulatory bodies are allowing BNPLs to go on with minimal regulation. This means they grow unfettered for now; however, risk is rising that Afterpay will be hit with regulation from the Reserve Bank next year that might allow merchants to pass on the cost to the users. This could be disastrous for BNPL platforms. The next frontier will be the USA and there is a fight in progress for a piece of that big American pie. How the regulation will play out in the USA will be key to their growth and pervasiveness in that market. Is BNPL on the cusp of a lending frontier? Will it help young people acquire safer access to credit, or is this just another pathway to higher levels of debt that can’t be paid back? Well, the good news is that at least the limits are low (for now) and there’s no high interest payments if you are late. I will be looking out for more partnerships between banks and FinTechs.

Just as I was editing this document, Afterpay has partnered with Westpac as Klarna has with CBA. Hopefully there will be more partnerships and less of the big banks buying out the FinTechs. I think the cooperation between the two will create a smarter open banking ecosystem more in tune with the needs of the evolving digital costumer.