Did you know that your favourite cafe does much more than satisfy your caffeine craving?

Small to medium enterprises (SMEs: less than 200 employees), like your local cafe, are the bedrock of the Australian economy. They are responsible for more than half of our GDP and employ a whopping 2/3 of the Australian workforce1. Naturally, SMEs rely heavily on banks to finance their operations, and most SMEs obtain loans from major banks.

However, small businesses encounter significant challenges accessing loans compared to large businesses. The COVID-19 pandemic widened this gap even further. For example, 25% of SMEs were unable to secure funding in 2020; and even worse, 40% received no financial advice from their bank during the pandemic. This has resulted in an all-time low trust in the major banks, with a trust rating of 2.26 out of 102.

Compounding the after-effects of the pandemic, the current macro-economic environment poses further challenges for SMEs. Inflation and rising interest rates are significantly impacting the ability of SMEs to regain control of their business operations. Recent findings suggest that two out of three SMEs are looking to secure new funding3. Given the all-time low trust in major banks and difficulties securing funding, SMEs will begin to explore other funding options besides major banks.

There is now a plethora of alternative funding options available to SMEs. Fintechs such as Moula, Prospa, and Lumi, are increasingly gaining traction in the market and are hungry to capture market share in the SME lending space. Unsurprisingly, a whopping 95% of SMEs have recently expressed openness to changing lenders for different or more competitive offerings4.

Now more than ever, major banks must consider that the only way to truly keep and grow their book is by becoming increasingly relevant to the customer. Banks need to progress from a traditional product-focused approach to a customer-focused approach in order to retain and grow their customer base.

So, how might banks better serve small-medium enterprises in this tumultuous environment?

The answer is by leveraging insights from customer data to drive interactions and provide a superior customer experience.

Using Insights from Data Analytics to Anticipate Customer Needs and Behaviour

Banks have access to a myriad of customer data. Trapped within that data are valuable insights – windows that provide glimpses into customer needs and behaviour. By leveraging data analytics, banks can predict customer behaviour, such as whether customers are likely to refinance their loan or respond to a new product offer. Data insights allow banks to focus on mobilising key initiatives to provide a superior customer experience via proactive engagement of customers at key touchpoints.

However, most banks lack a clear data analytics strategy that enables them to make the best use of existing customer data. It is not always clear as to where analytics efforts should be focused, what outcomes can be achieved, and what data to source.

To address these issues, we have identified key steps required to harness analytics and adopt a customer-centric approach.

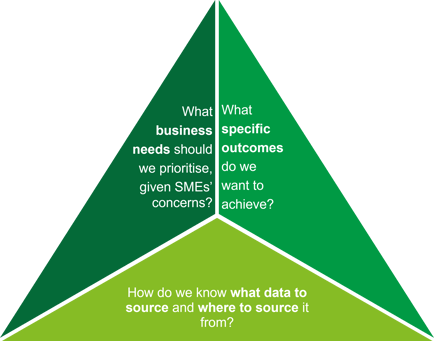

Figure 1. Key concerns our clients have expressed about using predictive analytics in SME banking

Figure 1. Key concerns our clients have expressed about using predictive analytics in SME banking

How Might We Use Predictive Analytics To Better Serve SME Customers?

1. Define what’s important to your business right now

Is high loan churn in the small business sector your main concern? Is it acquiring lucrative new SME customers in a particular industry vertical? Is it understanding which SME segments have the highest customer lifetime value? Is it reducing the time to ‘yes’ from days to minutes for business loan applications?While many problems can be solved using data analytics, narrowing your list and defining specific business scenarios will help maximise return on investment.

For instance, if customer attrition is a key concern, examples of business scenarios that could be addressed include:

- Retaining SME customers in specific industry verticals which require high regulatory navigation

- Retaining SME customers that have multiple options for refinancing with non-bank lenders

- Maximising the retention of customers who have been serviced for less than 12 months

Data insights will point to the specific solutions that may be most effective in each of these scenarios.

2. Determine what you want to achieve

Be specific as possible in the business outcomes you want to achieve. For example, if customer retention is your key business need, you may want to know:

- The likelihood of a customer refinancing a loan in the next 90 days

- The likelihood of a customer closing their account in the next 90 days

- The expected value at risk by a particular customer churning

Tie your business outcomes to the most pressing business challenges you want to solve.

3. Gather the data you need

Harness data sources that you already have and are authorised to use. Protecting customer privacy and confidentiality is paramount - extract only specific de-identified data points that you need to achieve your key business outcomes. Once these data points are determined, artificial intelligence (specifically, machine learning models) can be applied to predict your business outcomes.

Example internal data sources that you may be able to leverage are noted below (non-exhaustive):

- Customer relationship management (CRM) data: E.g., demographics, bank interactions (contact channels used, review sessions attended with a relationship manager, service satisfaction ratings, ratings, complaints made)

- Core banking platform data: E.g., financial position (loans taken, loan type, balance, assets to liabilities ratio), transaction history (anomalies in transaction method or transaction frequency)

- Accounting software data: E.g., cash flow (revenue and cost amounts, types), expense claims

- Credit decisioning software data: E.g., credit rating

- Payments processing platform data: E.g., products (cards held, card type, purpose), transaction history (purchase amounts, type, location, frequency, fraudulent activity propensity)

Note that the data points you need will depend on what has been shown in the past or in a similar industry to predict the business outcome you have identified. For example, research shows that specific data points across demographics, customer satisfaction, service usage, and macroeconomic conditions predict customer attrition. These data points can be captured using both internal and external data sources and used to create a machine learning model that predicts customer attrition.

Working with banking experts and data scientists will help banks to define:

- The most pressing needs of the business

- The specific business outcomes that can be achieved using analytics

- The data sources, types and models required to predict key business outcomes

Moving Forward with a Customer-Centric Approach

COVID-19 has severely impacted SME customers and undermined their trust in banks. This combined with the current economic situation presents a crucial opportunity to better serve SMEs moving forward. We propose that a key to mending this relationship is by leveraging insights from data analytics to predict SMEs behaviour and strategically mobilising initiatives that deliver a superior customer experience.

So, how exactly can we use analytics to predict customer behaviour? In part 2 of this blog, I deep dive into how predictive analytics can be used to address one of the biggest challenges in banking: customer attrition.

Stay tuned…

Want to learn more about customer analytics in banking? Read a short Deloitte report here.

Get in touch - Our Digital Banking team would love to hear from you!